In the investment world, understanding the balance between risk and return is critical for making sound decisions. This is precisely where the Bitcoin Sharpe Ratio comes in as an important metric that helps investors evaluate the risk-adjusted performance of their portfolios. So, what is the Sharpe Ratio, how is it calculated, and what does it mean for a highly volatile asset like Bitcoin? In this article, we will cover all the details.

What is the Sharpe Ratio?

The Sharpe Ratio is a risk-return metric developed by economist William F. Sharpe in 1966. Essentially, this ratio compares an investment’s return to the level of risk it carries. In other words, the higher the Sharpe Ratio, the more satisfactory the return provided relative to the risk taken.

The Sharpe Ratio is widely used in portfolio management and fund analysis. It considers not only the nominal return of an investment but also the extent to which that return involves risk. This allows investors to look beyond simply achieving high returns and assess at what cost those returns were obtained.

How is the Sharpe Ratio Calculated?

The calculation of the Sharpe Ratio is mathematically quite straightforward. The formula is as follows:

Where:

- R_p: Represents the return of the investment. For example, Bitcoin’s average annual return over a specific period.

- R_f: The risk-free rate. Usually based on government bonds or safe deposit returns offered by banks.

- σ_p (SD): The standard deviation of the investment, which measures the fluctuation in returns. The higher the standard deviation, the more volatile the investment.

In the formula, the excess return over the risk-free rate (R_p – R_f) is divided by the investment’s volatility (σ_p), measuring the excess return per unit of risk. For example, if the Sharpe Ratio is 2, the investor earns twice the excess return for each unit of risk taken.

What Does the Sharpe Ratio Tell Us?

The Sharpe Ratio shows how much return an investment provides relative to its risk. In this sense, it offers several critical insights for investors:

- Risk-Adjusted Performance: A high Sharpe Ratio indicates that the investment performs well relative to its risk. A low or negative Sharpe Ratio suggests that the investment’s risk does not justify the return or that the return is lower than the risk taken.

- Investment Comparison: It allows comparison of the risk-adjusted performance of different investment vehicles. For example, comparing the Sharpe Ratio of a stock with a bond portfolio can reveal which investment is more efficient relative to its risk.

- Portfolio Allocation and Diversification: The Sharpe Ratio shows risk distribution in a portfolio, helping investors assess the need for diversification.

- Benchmark Comparison: The Sharpe Ratio is also used to compare an investment’s performance against a reference or index. For instance, a stock fund’s Sharpe Ratio can be evaluated against benchmarks such as BIST 100 or S&P 500.

General Benchmarks for the Sharpe Ratio

A high Sharpe Ratio is generally viewed positively. Commonly accepted values in the financial world include:

- Sharpe Ratio around 1: Acceptable risk-return balance.

- Between 1 – 2: Good risk-adjusted return.

- Above 2: Excellent risk-adjusted performance.

- 0 or negative value: The investment is not worth the risk or provides lower return than the risk taken.

However, these values are not context-independent; market conditions, investment horizon, and volatility directly affect the ratio.

Limitations of the Sharpe Ratio

Although the Sharpe Ratio is a powerful tool, it has some limitations:

- Source of Risk: The Sharpe Ratio only shows the risk-return balance; it does not indicate where the risk originates. For example, it is not clear whether a portfolio’s risk comes from a single volatile asset or from many diversified assets.

- Market Conditions and Management Style: When comparing Sharpe Ratios of different funds, factors such as market conditions, liquidity, or management strategies are not taken into account.

- Volatility-Based Measurement: Standard deviation assumes normal distribution. However, financial markets are often exposed to extreme tail events, which can cause the Sharpe Ratio to not fully reflect the risks.

- Serial Correlation Issue: Returns may be dependent over time. This can make volatility appear lower and the Sharpe Ratio higher than it actually is.

For these reasons, the Sharpe Ratio should be used together with other metrics for portfolio analysis and risk assessment rather than as a standalone decision tool.

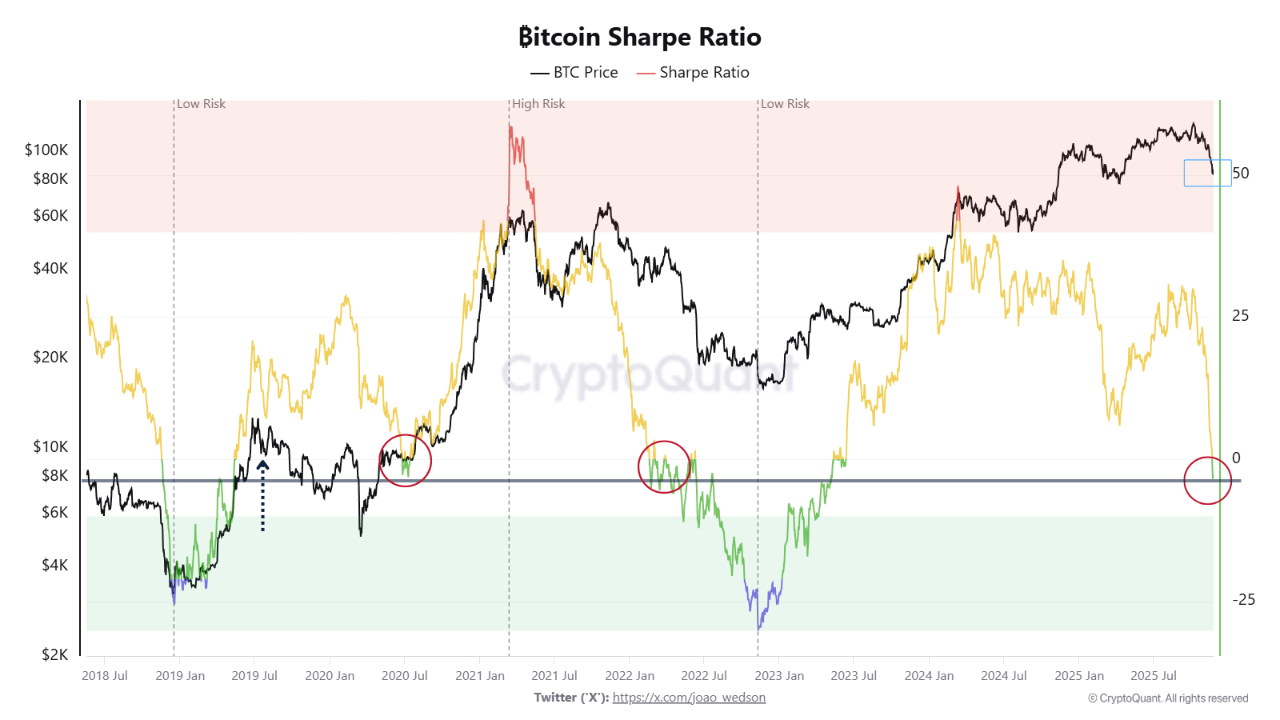

Why is the Sharpe Ratio Important for Bitcoin Investments?

Bitcoin is inherently a highly volatile asset. Daily price fluctuations and sudden market movements create both opportunities and risks for investors. This is exactly where the Bitcoin Sharpe Ratio helps investors measure the risk-return balance.

- Importance of Volatility: Bitcoin’s standard deviation is quite high. This indicates significant short-term price fluctuations. The Sharpe Ratio uses this volatility as a risk measure.

- Risk-Adjusted Excess Return: Since Bitcoin’s return is usually above risk-free investments (e.g., government bonds), the Sharpe Ratio allows investors to see whether the excess return justifies the risk taken.

- Investment Decisions: A high Sharpe Ratio means Bitcoin provides satisfactory returns relative to its risk. A low or negative ratio indicates that the investment does not adequately compensate for the risk.

How to Interpret the Bitcoin Sharpe Ratio?

When interpreting the Sharpe Ratio for Bitcoin, pay attention to the following points:

- High Sharpe Ratio: Indicates that BTC provides high returns relative to its risk. This is a positive signal for investors with high risk appetite.

- Low or Negative Sharpe Ratio: Bitcoin, despite being a risky investment, does not provide sufficient return. This serves as a warning for risk-averse investors.

- Price Fluctuations and Market Conditions: The Sharpe Ratio is based only on past performance. Regulatory news, macroeconomic fluctuations, or institutional adoption can increase or decrease Bitcoin’s volatility and thus affect the Sharpe Ratio.

- Time Horizon: Bitcoin’s Sharpe Ratio can vary in short and long terms. Long-term investors may see a high Sharpe Ratio despite short-term volatility.

The Connection Between Sharpe Ratio and Bitcoin Investment

As Bitcoin’s popularity in the investment world has increased in recent years, the importance of risk-return analysis has also grown. With the Sharpe Ratio, investors can:

- Compare Bitcoin’s risk in their portfolios with other assets.

- Optimize investment decisions based on risk-return balance.

- Analyze Bitcoin’s performance over different periods to form long-term strategies.

For example, if Bitcoin’s Sharpe Ratio is around 2, the investor has earned twice the return per unit of risk. However, if the Sharpe Ratio is 0.5 or negative, the investor is not adequately compensated for the risk taken.

Strategic Considerations Regarding the Sharpe Ratio

Bitcoin investors can draw some strategic insights when using the Sharpe Ratio:

- Portfolio Diversification: If Bitcoin has low correlation with other assets, it is possible to reduce portfolio risk using the Sharpe Ratio.

- Long-Term Perspective: Short-term fluctuations can affect the Sharpe Ratio; therefore, long-term investors should consider long-period averages.

- External Risks: External risks such as regulation, security breaches, or technological failures can suddenly lower the Sharpe Ratio. Relying solely on historical data for decisions can therefore be misleading.

Bitcoin Sharpe Ratio Example

One of the best ways to understand the Sharpe Ratio is through real investment scenarios. Suppose we compare two cryptocurrencies: Bitcoin and Ethereum. Although both have provided significant returns in recent years, Ethereum’s price fluctuations are higher than Bitcoin’s.

- Bitcoin: Expected return 20%, standard deviation 30%

- Ethereum: Expected return 30%, standard deviation 50%

- Risk-free rate: 2%

When we evaluate both assets using the Sharpe Ratio formula, even though Ethereum’s nominal return is higher than Bitcoin’s, its risk-adjusted return remains slightly below Bitcoin’s due to higher volatility.

This situation allows investors to make choices based on their risk preferences:

- Those seeking a more stable and risk-efficient investment may prefer Bitcoin.

- Those willing to take higher risk for potentially higher returns may turn to more volatile assets like Ethereum.

This example clearly illustrates how the Sharpe Ratio goes beyond just looking at returns and also shows how effectively risk is managed.

You can also freely share your thoughts and comments about the topic in the comment section. Additionally, don’t forget to follow us on our Telegram, YouTube, and Twitter channels for the latest news and updates.